The ACA worked, so Wittman broke it (Part 1)

Skyrocketing healthcare costs are the direct result of the scheme to ruin the ACA

Welcome to the Wittman Watch newsletter!

Last week we wrote about the challengers for the VA-01 congressional seat. UPDATE: As of this writing, Lisa Vedernikova Khanna has withdrawn from the race, and Lewis Littlepage has declared his candidacy.

Scroll (way) down to see our social media roundup for the week.

Hi 👋 to our many new subscribers! Check out our About Us, and find some of our previous social media posts in our Archive.

We think this topic is worth covering thoroughly — it’s vitally important to understand how we got to where we are with the ACA and healthcare, and it’s so relevant to what’s going on now. Since this is a long article, we’ve split it up into two parts.

This is Part 1. Part 2 is right here.

The story of how an effective program was deliberately undermined (Part 1)

As the expiration of ACA extended subsidies cut thousands of Americans off healthcare and massively raise premium prices, some folks in the comments of our social feeds have been saying things like this:

On December 4, 2025, Rob Wittman stated that US healthcare is neither transparent nor affordable; that reform is needed; and that he has the prescription to solve everything. His message is an excellent example of how Congressional Republicans create problems and then demand “reform” to fix the problems they created… and the “reforms” often make the problems even worse.

Wittman and this commenter make two accusations:

Misconception #1: The ACA only succeeded in inflating insurance prices

Misconception #2: ACA subsidies were intended to sunset

Without context, these sorts of comments might pass as reasonable positions. But all becomes clear when history is examined: these accusations are propaganda that has been carefully cultivated by people like Rob Wittman, whose interests are to shunt us all to expensive private healthcare plans, or throw us off our healthcare plans entirely.

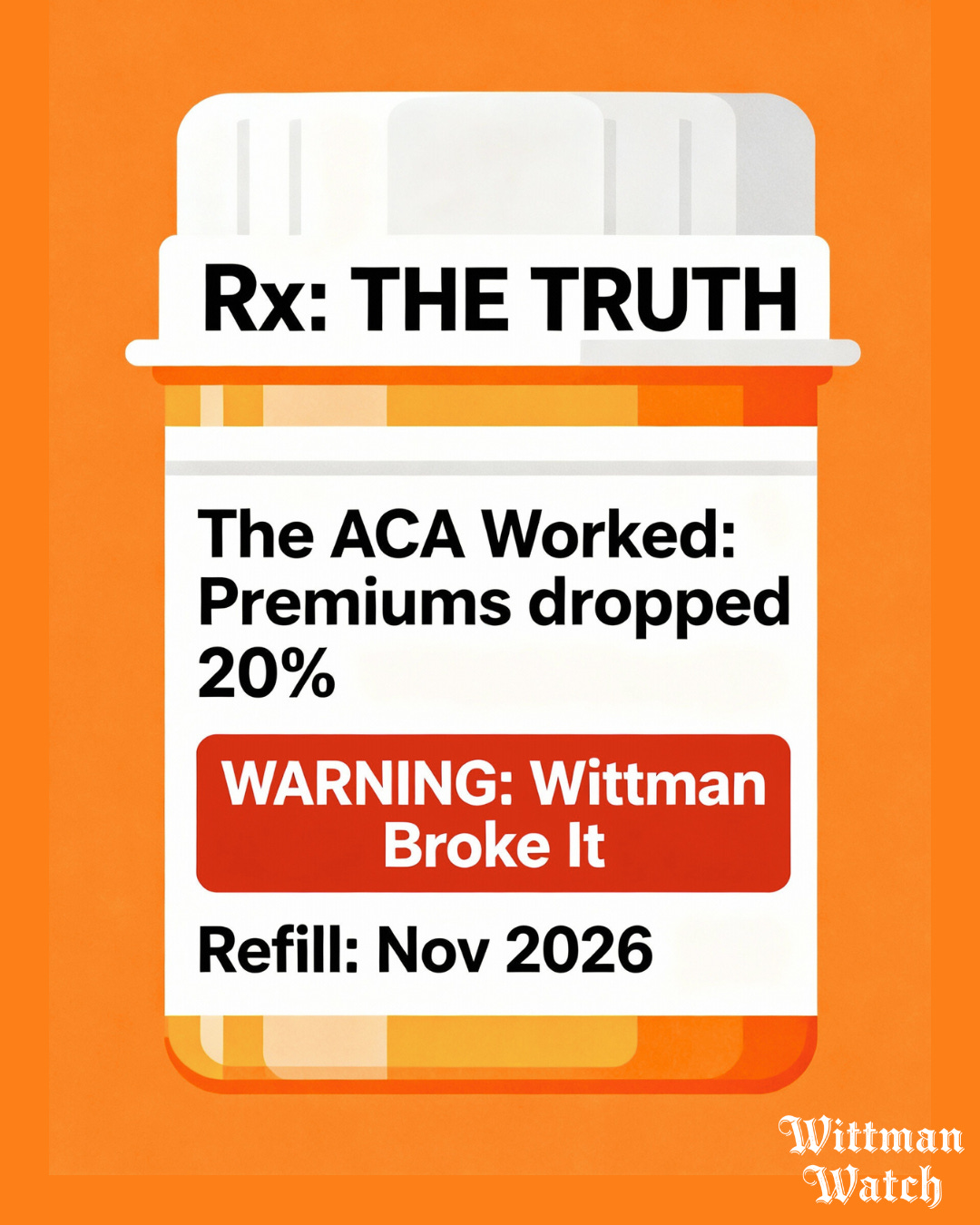

The ACA made premiums drop by ~20%

First we need to state something clearly: Before the ACA, individual market premiums rose an average of 10% or more every year. The ACA reversed this trend: 2014 premiums were 10-21% lower than 2013 pre-ACA individual market premiums, even as the quality of coverage improved and more people got access to healthcare. The ACA slowed the rate of premium growth significantly compared to pre-ACA trends. But then healthcare insurance lobbyists — with the help of Republican politicians like Wittman — started messing with the program, successfully undercutting the basis on which these achievements had been built. For example, the elimination of the individual mandate in 2017 (effective in 2019) contributed to premium increases of 8-10% and reduced enrollment by millions.

How did we go from the program being highly effective and significantly reducing premium costs, to a healthcare environment with premium costs spiraling upwards?

Time for a history lesson: The ACA was based on a Heritage Foundation idea

The ACA did not introduce a brand-new economic model for healthcare. Instead, it nationalized the program piloted by then-Governor Mitt Romney in Massachusetts, which was itself built upon a framework proposed by Stuart Butler at the Heritage Foundation to preserve private insurance markets. (We note that some sources — especially those backed by Koch money — argue this is less-true or not true at all. Our source is Politico, which is center-left and rated highly on factual accuracy.)

Heritage preferred and promoted Butler’s model because they did not want a single-payer system, such as an expansion of Medicaid, and demanded that people have “personal responsibility” over their own healthcare by buying health insurance in a fair market. The Butler/Heritage model, which Romney implemented in Massachusetts, relied on three points:

Guaranteed Issue: Insurers must issue coverage to everyone, including those with pre-existing conditions

Individual Mandate: Everyone must buy insurance

Subsidies: Ensure people with low incomes can afford the individual mandate

The bottom line is that the continuation of the US health system’s reliance on health insurance companies was not an idea from the political left, but was in fact exactly what the leading conservative think tank proposed and preferred.

Calculated destruction of the ACA

“Free market purism” is the belief that, when left to their own devices (that is, when they are unregulated and left to self-govern), markets will automatically produce the most efficient outcomes. This is a bulwark of American conservatism. (We won’t debate this belief here; suffice it to say we think it’s deeply flawed, naive, and quite possibly deadly.) The ACA was regarded as an affront to this notion of free market capitalism. That’s why conservative politicians responded willingly to lobbying from the healthcare industry, and they began to undermine, attack, and sabotage the ACA. Under Trump in 2018, the Republican Party did this in three ways:

Eliminating cost-sharing reduction (CSR) payments

Creating market uncertainty (as insurers priced in potential losses)

Passing the Tax Cut and Jobs Act in 2017 that eliminated the individual mandate penalty, which took full effect in 2019

Let’s take these one at a time.

1. Insurers shifted the cost of higher risks to everyone’s premiums

The elimination of CSR payments was the first domino to fall. CSR payments — unlike the subsidies, which were tax credits — reduced the cost of obtaining healthcare services by lowering deductibles and copayments for certain lower-income enrollees. When these payments were eliminated, insurers still had to cover their costs… so they increased the premiums for Silver plans on the ACA. In other words, Trump’s elimination of CSRs just dumped the increased healthcare costs back on consumers through increased premiums. In turn, these increased the premium tax credits for which enrollees might be eligible. The Kaiser Family Foundation predicted that if Trump had simply left CSR payments alone, it would have cost taxpayers $2.3bn less! Regardless, the uncertainty about CSR payments meant that insurers raised premiums.

What were the results? Benchmark Silver plan premiums surged 36% nationally. The repeal of the individual mandate increased the likelihood of being uninsured by 0.5 percentage points (a 24% relative increase). RAND’s analysis projected 12.3 million fewer people insured and 8% increase in premiums.

2. Without the individual mandate, healthy people stopped buying insurance

By the time all this was happening, Romney was a US Senator. He argued that his use of an individual mandate in the Massachusetts program was acceptable because that was a state-based program, but that it was an overreach for the federal government to make it the law of the nation. He and his party knew that eliminating the individual mandate would crush the ACA’s ability to function, and they destroyed it anyway.

“So what?” you may say. “Why would the individual mandate matter so much?” It’s all about risk management. Generally speaking, insurers place individuals into “risk pools.” These are groups of people who will need more or less medical care or, put another way, they’ll cost the insurer more or less money depending on their likely healthcare needs. The mandate’s purpose was to require healthy individuals to participate, spreading risk across a balanced pool of insured people. Without the mandate, young and healthy folks dropped their coverage, leaving a sicker, more expensive population that drove up per-person costs. And now we all reap the results.

3. Subsidies were not extended because billionaires needed yachts

The ACA subsidies were always intended to be a permanent part of the program, contrary to our Facebook commenter’s belief. They were capped at certain income levels, based on household size and configuration. The subsidies ensured that everyone could buy insurance by subsidizing lower income households, spreading the risk across a larger pool of people, thus lowering prices for everyone.

As the nation dealt with COVID, healthcare costs spiked for everyone while, at the same time, inflation rates were skyrocketing. To provide temporary financial relief for those who might otherwise struggle to afford premiums and medication, Biden increased the income caps for ACA subsidies. These increased caps were scheduled to expire at the end of 2025. Even though Trump campaigned on “affordability,” his administration chose to let these extended subsidies expire, while handing huge tax cuts to the wealthy. As of this writing, there are no extended subsidies for people who buy insurance from ACA exchanges. (On January 8, Wittman voted on a bill to extend the subsidies for three years — a bill that everyone knows is already dead in the water.)

To recap: Republicans/Wittman/Trump knew the ACA was working, that premiums were coming down, and that more people were insured. But by eliminating the individual mandate and cutting CSR payments, they guaranteed that premiums would increase, fewer people would be insured, and the ACA would look like it was failing. And most recently, by failing to bring the expiring subsidies to a vote before the end of 2025, they chose not to address healthcare affordability at all.

To be continued…

What do you think about the ACA, the current fight over healthcare, and Wittman’s actions around it? Comment here or on Facebook, Instagram, BlueSky, or Reddit.

As seen on our socials

Our social media channels respond quickest to whatever Wittman does or says. Here’s a selection from the past week. Click on each post to see them on BlueSky (no account necessary). Follow us on BlueSky, Facebook, Instagram, and Reddit to get immediate updates each time we post.

That’s a wrap

Please subscribe and share our (always free) content with your friends!

This November, we’ll make sure our seat is filled by someone who’ll work for us.